Since the end of 2014, the stock market has increased over 13% per year . . . one of the best decades in investing history. During that same period, the Kansas City Chiefs made the playoffs each year, winning three Super Bowls along the way.

Coincidence? Let’s hope so . . . because the Chiefs were just eliminated from the playoffs this past week, and if there is any merit to the connection, we could be in for a rough year of investing.

Jokes aside, even here in Kansas City we don’t think there’s any investment magic associated with Patrick Mahomes & Co. But here we are at the end of 2025, and today seems as good a time as any to look back on this year and how it treated us as investors.

January started with a lot of concern about the incoming president. Upon inauguration, Donald Trump unleashed a flurry of high-impact policy actions and executive orders. In our February Investment Commentary, we again reminded clients that “the president of the United States gets way too much credit when the economy is good and way too much blame when the economy is bad—that there are much larger forces at work determining our financial fate.”

However, Trump was enacting such dramatic policy changes regarding tariffs/international trade, budgets, and immigration that we started to question our own adage. Could this time be different? Ultimately, we concluded, probably not.

And that’s basically how the year went. There was a lot of noise and volatility, but ultimately, things that were significant concerns on Inauguration Day have not yet panned out to be problematic from an investment standpoint.

On April 4th, or “Liberation Day,” Trump stunned investors and sparked a significant selloff in the stock market when he announced huge and unprecedented tariffs on basically every country that could fog a mirror. The S&P 500 Index, which had already been on the decline, traded down 19% from its February peak. Down 20% would have been considered “bear market” territory.

The president nearly caused a bear market? Is this time different?

For a brief moment, the answer was . . . umm . . . yes?

But in reality, no. This time is not different. Eventually, the massive “reciprocal” tariffs were walked back by the administration. Concessions were made, deals were struck, and the market got over it. There is lingering concern that the (much reduced) tariffs still in place could cause some problems, but for the most part the market has shrugged it all off. Like it almost always does. Heck, the tariffs could still go away entirely if it turns out they are illegal. More on that later.

Elon Musk and DOGE (the Department of Government Efficiency) also caused a lot of ruckus in 2025. Whether Musk did it the right way or not, we applaud the attempt to tackle our nation’s budget problem. However, DOGE, predictably, just came and went. Our government spends nearly $2 trillion more than it takes in every year. Even if DOGE was cutting tens of billions from the budget, a billion dollars just ain’t what it used to be.

The One Big Beautiful Bill Act (OBBBA) was passed in July. While it may support higher economic growth, it also is expected to add to our debt problems. Again . . . whether you like Trump or not, this was just more continuation of the same from previous administrations. Increased spending and more debt.

The stock market hardly batted an eye in response to the OBBBA, but the bond market did get a little heartburn. Treasury bonds declined a bit over concerns of rising debt levels, but even that was short lived. This time is not different. Politicians, red and blue, have a proven track record of racking up debt. And investors don’t seem to care.

2025 also saw the longest U.S. government shutdown in history. Yet the market, flying blind with a dearth of economic data owing to the shutdown, just yawned.

The effect of Trump’s immigration policies on the economy is still TBD. From a purely economic viewpoint, agnostic of the rightness or wrongness of the policy, the concern is that mass deportations and strict immigration will lead to fewer people in our economy. And fewer people spending/working/participating in our economy should eventually stymie growth. But somehow the United States continues to defy any and all economic kryptonite . . . year . . . after year . . . after year. President . . . after president . . . after president.

Amid all of this drama in 2025, investments had a good year all around. U.S. stocks are up almost 12% (Equal-Weighted S&P 500 Index). International stocks, even with all the tariff noise, did even better, up 30% (MSCI All Country World Index ex-U.S.). And bonds are having their best year since 2020; the Bloomberg U.S. Aggregate Bond Index is up over 7%. The best-performing asset class? Precious metals. Anyone with an allocation to gold has been happy with its 65% price increase this year.

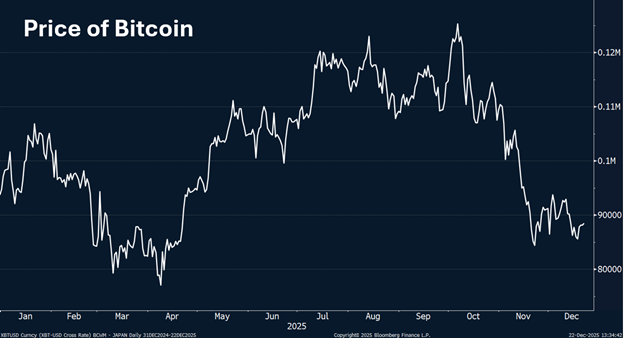

Bitcoin, while only down 5% for calendar year 2025, has plummeted from its peak just two months ago, falling almost 30%. Although investing in currencies (any currency) has not been a priority for BCWM, we clearly try to avoid investments that produce no cash flow (dividends or interest). We also try to avoid “investments” that have the potential to drop 30% in less than two months.

So . . . we repeat . . . this time is NOT different. The president of the United States gets way too much credit when the economy is good and way too much blame when the economy is bad. There are much larger forces at work.

In April 2024, when artificial intelligence (AI) was more curiosity than commonplace, we tried to explain what it was . . . and what it wasn’t. We also reminded our readers that, while we may be on a trajectory toward ever more powerful machines, we were not, at least not yet, on a direct path to the Terminator traveling back in time from a post-apocalyptic 2029 to kill Sarah Connor.

Fast forward to 2025, and even though the Terminator has still not yet arrived, AI has. This was the year that AI went very much mainstream.

At first, this new technology felt a bit like a party trick. “Watch this thing write a poem.” “Check out this photo of a cat in a tuxedo.” In 2025, AI started becoming a tool people used in everyday life. Analysts estimate that nearly 1.8 billion people worldwide have used AI tools, with 500–600 million engaging with them daily. In the U.S. alone, more than half of adults report actively using AI, and roughly one in five use it every day, many of them multiple times, for writing, planning, analyzing, creating, and more.

It has seeped into our search engines and operating systems such that sometimes you don’t even realize you are using AI.

Building AI at scale has required enormous upfront investment. Several of the largest technology companies, who previously relied on cash flow to fund these types of capital expenditures, have turned to the bond market, recently issuing tens of billions of dollars in new debt. The sheer size and frequency of the issuances unsettled parts of the market, raising questions about capital discipline, returns on investment, and how long the spending spree might last.

Looking ahead to 2026, the question will move from how much is being spent to what that spending is producing. We expect the market to be more discerning about rewarding companies that demonstrate not just investment in AI, but a return on that investment.

Another story we will be watching is the ongoing tariff saga. As hinted at above, part of the uncertainty has simply been kicked down the road. Several of the remaining tariffs are now facing legal challenges, with the Supreme Court set to weigh in on whether the administration even has the authority to impose tariffs in the first place. Costco has already sued over the issue. That sets the stage for another round of headlines, court dates, and political and legal theater. Just another year in the life of Donald Trump.

Most importantly, though, we will be watching data into 2026 to ascertain what economic path we are on. After flying blind through the shutdown, this week we got a peek at some long-awaited data that confirmed what we already surmised: the job market is waning and inflation is receding. Not necessarily the best setup for another double-digit year of stock market growth, but then again, we’ve said that before.

This information is provided for general information purposes only and should not be construed as investment, tax, or legal advice. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable but is not guaranteed.