It seems that whenever there is new and unusual financial turmoil in the world, the value of the dollar is frequently listed as an eventual victim. Maybe this time it’s true. Maybe this time the dollar will cease to be the world’s reserve currency. Maybe this time some other nation or nations (the BRICS?) or some cryptocurrency or precious metal or whatever will replace the U.S. dollar as the primary means of financial exchange worldwide.

Or maybe not.

We don’t mean to beat a dead horse here (and this is a very dead horse), but just because the dollar trades down in value (relative to other currencies) doesn’t mean the world’s financial order is about to be upended.

To put this in perspective, below is a graph of the dollar index for the past 59 years.

We heard some pundit on CNBC make the comment (somewhat dramatically) that the dollar is trading at a 4-year low. Which is true. What he did NOT say is that the dollar is trading at almost the same exact level as forty years ago! Some years it has been higher (2001) and some years it has been lower (2008 . . . The Great Financial Crisis), but net-net-net, today it is trading at about its average price for the past forty years.

SO BORING!

Meanwhile what is not boring is the price of precious metals . . . such as gold and silver.

Gold and silver have been on a tear, increasing 64% and 149%, respectively, in calendar year 2025 – and even more in 2026.

Many investors still refer to gold as an inflation hedge. But with inflation running at a modest 2.7%, that explanation doesn’t hold much water.

We’ve said it before and we’ll say it again: Gold is not an inflation hedge. It’s an uncertainty hedge.

Uncertainty being a very vague term describing a population’s emotions regarding a variety of issues – political, financial, military, meteorological, geo-political, basically everything in the world. The uncertainty initially driving this rally in precious metals has been described as lost faith in the U.S. dollar owing to massive budget deficits and volatile U.S. trade policy.

Nevertheless, some “investors” (we use that term loosely) have turned gold into a speculative trading vehicle.

And silver as well.

And don’t forget copper.

And of course, cryptocurrency.

But whenever investors start talking about a new financial world order – and congratulating themselves for having seen it coming, it’s worth taking a breath. Markets have a long history of humbling those who think they’ve decoded the future.

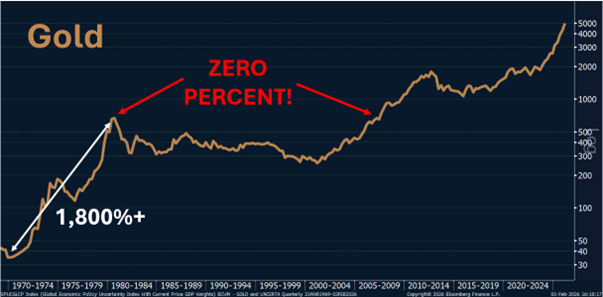

Below is a 57-year graph of gold prices. Back in the ’70s (when there was high inflation), gold was on fire, increasing over 1800%.

And then over the next twenty-five years, gold had a net return of zero percent. That’s right . . . ZERO PERCENT! For twenty-five long years. From 1980 to 2005, gold actually declined in value just a tiny fraction of a percent.

Twenty-five years is a long time to wait for a return and get absolutely nothing.

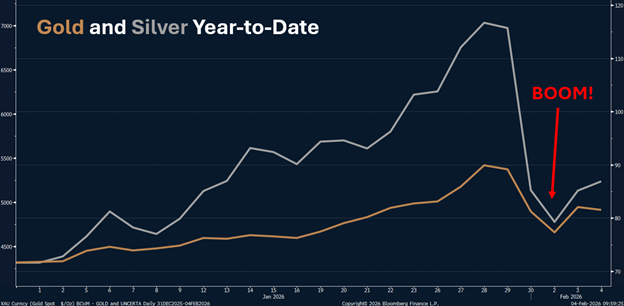

After the incredible rise of precious metals in 2025, gold and silver had a meteoric first twenty-eight days of 2026, rising 25% and 63% respectively. But just when you thought about putting every nickel you owned into gold and silver . . . BOOM, they were down 14% and 32% in just three days.

Have they had their fun? Is it over? Who knows? But we would hate to hold them for the next twenty-five years and get a zero percent rate of return.

We would be inclined to say “thank you very much” to gold and silver and move most of our investments into something that produces profits and dividends (cash flow).

Stepping back to assess this madness, one could argue the recent moves in the dollar and commodities markets are somewhat justified. Today’s world seems much more uncertain than it was a year ago. And the year before that.

But it’s not an impending disaster for your investments. Our economy is robust, our national resources are bountiful, and there is a silver lining to a cheaper dollar. . . it means we’ll sell more stuff to foreigners.

And then there’s Bitcoin. Poor misunderstood Bitcoin, which has turned many people into multi-millionaires over the past decade and probably quite a few into paupers in recent months.

Since Bitcoin peaked last October at $126,000+ it has declined 50%, trading lower than $63,000 as recently as Thursday evening.

Long, long ago, Bitcoin and crypto evangelists told us how this new technology was going to revolutionize the world. Crypto “currencies,” “projects,” and “startups” popped up out of nowhere to create an ecosystem for the new world order. The blockchain! NFTs! It was a wild and confusing time.

Before long, it became obvious that this future was just a pipe dream. However, the crypto believers that stuck around quickly changed their tune. Maybe the world wouldn’t run on the blockchain, but Bitcoin should really be viewed as a sort of “digital gold,” they said. It was billed as a new safe-haven store of value for global transactions that the government can’t get its hands on.

It hasn’t acted much like gold recently. . .

. . . wonder what they’ll say next?

Reminder: Bitcoin doesn’t pay a dividend because it has no business and creates no profits. Bitcoin also doesn’t pay any interest. So, the value of Bitcoin is . . . well, we don’t know what it is. No one knows what it is. And there is a possibility that no one ever will know what it is.

We hesitate to say “NEVER EVER,” but we cannot foresee a time where Bitcoin will be any part of our clients’ portfolios.

_______________________

With all the headlines recently (financial and otherwise), it has been easy to forget about Trump’s tariffs. A little less than a year ago they were causing all kinds of anxiety in the stock market. What has been the fallout?

For starters, tariffs generated $287 billion in revenue last year. Unsurprisingly, this number is way higher than the roughly $100 billion collected in 2024, when Trump was not in charge. Since the tariffs are fees charged to importers of foreign goods, U.S.-based businesses are the ones forking over the $287 billion. The concern is that those businesses will eventually raise their prices on the end consumer, which would then push inflation higher.

While some inflation pressure did show up in the prices of goods, overall inflation in 2025 (2.7%) was lower than in 2024 (2.9%). That’s right. Inflation went down! Prices still rose (as they almost always do), just not by very much.

Concerns about tariff-driven inflation are easing. Good news.

What about the tariffs’ impact on our government’s massive debt problem? Did it help?

Well, yes. A little bit. Our deficit (the amount we overspent) shrunk – from 1.82 trillion in 2024 to 1.78 trillion in 2025 (an improvement of about $40 billion). That still means total spending increased overall. Without the $287 in tariff revenue collected, the budget deficit would have been worse.

So, no real meaningful improvement to our national debt. But at least it got worse at a slower rate.

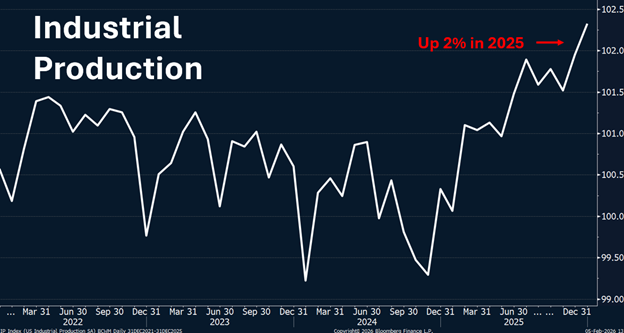

What about manufacturing? Forcing companies to “Buy American” should have helped American factories, right?

Again, the results are mixed.

On the one hand, after several years of decline, industrial production increased by 2%. Factories are finally producing more stuff.

On the other hand, factory workers continue to lose their jobs — approximately 70,000 in 2025, continuing a decades-long trend.

So maybe that’s why tariffs haven’t gotten much attention lately. While they seem to be helping Trump exert leverage on other countries, compelling them to begrudgingly come to the negotiating table, their impact has been otherwise – just been kind of “meh.” The scary things (higher inflation) have not materialized, and the proposed benefits (lower deficits and a manufacturing resurgence) have not been impressive.

Bottom line, the tariffs haven’t really moved the needle.

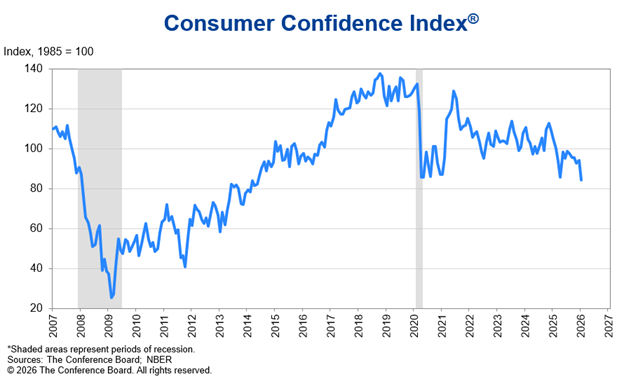

Consumers are the most important factor moving the needle in the U.S. economy. Are they worried? Are they optimistic about the future? Are they spending? Will they spend more? And more? There’s a lot of fuss regarding the psychology of the American consumer, and for good reason. Spending drives our economy.

Last month, one measure of consumer confidence fell to its lowest level since 2014. The survey tracking this data asks Americans how they feel about their finances and the economy. Confidence levels in this lower range have historically been associated with periods of softer economic growth.

Yet the economy appears to be doing well. The “GDPNow” tracker produced by the Federal Reserve Bank of Atlanta points to fourth-quarter growth running at a 5%+ annualized pace. This is an incredibly strong figure and a lot of that growth has been powered by consumer spending.

So why does spending look strong while consumer confidence seems weak?

Part of the explanation lies in who is driving spending. Since the pandemic, wealthier households (who own the majority of financial assets) benefited disproportionately from rising home prices and the AI-driven stock market.

Meanwhile, many middle- and lower-income households, which depend more on wages than asset values, feel ongoing pressure from the higher cost of goods and services, and their net worth remained stagnant.

Since the top 10% of earners in America account for about half of consumer spending, the result can be a strong economy even if confidence readings suggest otherwise.

Markets and GDP respond to actual spending, not sentiment, and right now, actual spending remains just fine.

This information is provided for general information purposes only and should not be construed as investment, tax, or legal advice. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable but is not guaranteed.