The Federal Reserve got itself a new leader this past month as Kevin Warsh took over as chairman, replacing the beleaguered Jerome Powell.

“Beleaguered,” because Mr. Powell and President Trump never seemed to agree on the proper level of interest rates . . . whatever that might be.

The president has long preferred lower interest rates, which generally stimulate economic activity, encourage borrowing, and tend to be supportive of stock prices (at least in the short run). And strong markets typically lead to positive election results for sitting presidents.

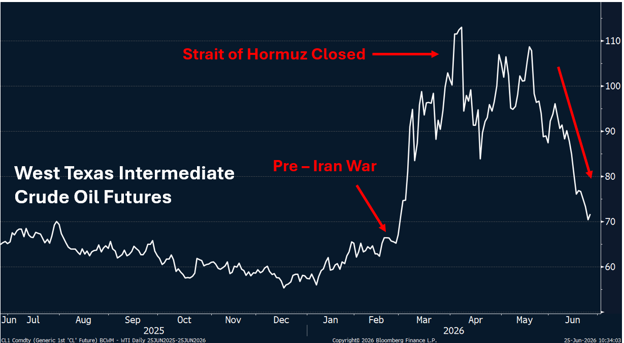

Unfortunately, Mr. Powell was kinda between a rock and a hard place. While being pressured by the president to reduce rates, he was also dealing with a whiff of inflation resulting from the president’s decision to start a little skirmish with Iran, causing oil prices (and the cost of everything oil touches) to go up.

Mr. Powell found it difficult to reduce interest rates at a time when he felt he might actually need to INCREASE rates.

Enter Mr. Warsh, who is allegedly more sympathetic to our president but is also good at doing math. And when Warsh started his job, the war was still going strong and the math was pretty clear: cutting interest rates was likely premature.

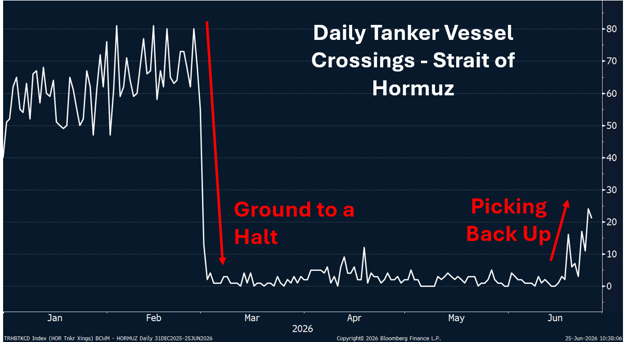

Fortunately, the equation may be changing almost as quickly as it developed. The Trump administration reached a preliminary agreement with Iran, and commercial oil tanker traffic has begun flowing through the Strait of Hormuz again. The number of ships going in and out of the Strait had ground to a halt in March and has begun picking back up.

Consequently, the price of oil, which almost doubled when the Strait closed, has decreased this month to roughly where it traded before the conflict began.

And that’s important, because energy prices find their way into the price of almost everything . . . from airline tickets to groceries to the package sitting on your front porch.

Higher energy prices from earlier in the year are showing up in inflation numbers released this month. Consumer Price Inflation was up 4.2%, the highest level in three years.

Will we see a corresponding decrease in inflation as the Strait (hopefully) stays open and oil prices settle back to their pre-war levels? Maybe. But that is precisely the Fed’s problem: inflation data looks backward, while decisions about interest rates are meant to look forward.

So, Chairman Warsh inherits a wonderful dilemma. The inflation report says, “Don’t cut yet.” The oil chart says, “Maybe calm down.” And the White House likely says, “Cut anyway.”

Welcome to the job.

Speaking of the Fed, former Federal Reserve Chairman Alan Greenspan, who led the central bank from 1987 to 2006, passed away this week at the age of 100. Central bankers have a well-earned reputation for saying a lot without saying too much. The art of “Fed speak” is to leave every possible policy option on the table while convincing everyone you said something profound.

No one mastered that craft better than Greenspan. During Senate testimony in 1987, he reportedly remarked:

“If I seem unduly clear to you, you must have misunderstood what I said.”

In one sentence, he explained decades of Federal Reserve communication.

Priceless!

This information is provided for general information purposes only and should not be construed as investment, tax, or legal advice. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable but is not guaranteed.