Imagine ten buildings, each the size of seven football fields, clustered together on a campus the size of Central Park, humming with enough power to run a city of a million people. That’s the Stargate data center in Abilene, Texas . . . one of many more such sites that will be built in Chat GPT-creator OpenAI’s “Stargate Project,” a $500 billion bet on building the world’s biggest AI factories. In partnership with Oracle, SoftBank, and now Nvidia, OpenAI plans to construct massive new data centers packed with supercomputers to train the next wave of AI brains in pursuit of “artificial general intelligence” (AGI). A much more sophisticated intelligence that, in theory, could mirror human cognitive abilities (although recently that seems to be a rather low bar).

This is cool (and maybe a little scary). Building AI factories of this scale is not just a technological leap; it’s a potential economic transformation. The implications are enormous but also unpredictable. One thing is certain: these buildings are going to require a lot of energy, making their environmental footprint a subject of intense debate.

The AI boom that started with ChatGPT has rippled far beyond Silicon Valley. The “Magnificent Seven” stocks have surged since the term was coined in 2023, while utility companies are now riding a wave of new demand as data centers strain an aging power grid. At BCWM, we own positions in both camps: the Mag-7 names that helped fuel this rally, and power companies that stand to benefit from AI’s insatiable appetite for electricity. But we’re also cautious. With much of the excitement already baked into prices, we’ve been trimming positions selectively as valuations stretch higher.

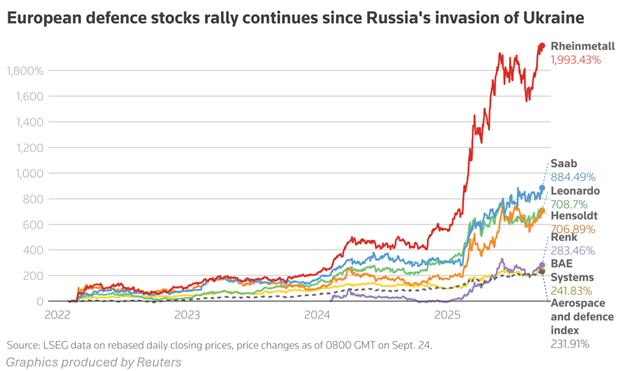

Interestingly, while the Magnificent Seven have dominated headlines since 2022, another subset of stocks has quietly outperformed even these giants of the market. Ones you never hear about. European defense stocks tell a striking story. Rheinmetall, Europe’s largest ammunition producer, has surged nearly 2,000% while the broader European aerospace and defense index has tripled in value since the Russia–Ukraine war began.

Adding to their momentum are recent comments from President Trump.

He acknowledged Ukraine could reclaim all territory occupied by Russia, agreed that NATO should shoot down Russian aircraft that violate its airspace, and said U.S. weapons sold to allies can be given to Ukraine. Those remarks underscore how the conflict remains very much unresolved and how the geopolitical climate could continue to fuel strong demand for the defense sector. We own two names in defense: Lockheed Martin (LMT) and Northrop Grumman (NOC) and wouldn’t be opposed to owning more. Unfortunately, defense stocks will never go out of fashion.

People have FOMO about not being in the hot new tech stocks. But you never hear someone say, “Why didn’t you buy SAAB?!”

After a long wait and much debate, the Federal Reserve finally cut interest rates for the first time this year. The move is intended to subtly support the economy and the waning job market.

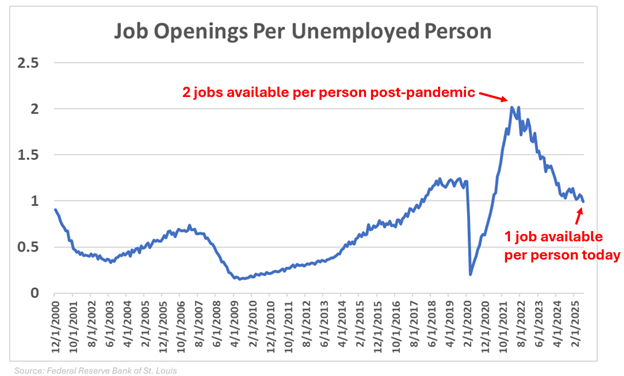

That’s not to suggest that the labor market is in bad shape. Unemployment is rather low (4.3%) and there is about one job opening available for every unemployed person. However, it is trending in the wrong direction. Three years ago, there were two jobs available per unemployed person.

Looking at the chart above, you can see that we still have more jobs available per unemployed person than most of the twenty-five-year history this data has been collected. And, you can argue that having fewer jobs available can help control inflation (fewer jobs = lower wage-pressure from employees).

So, while the job market has been softening, it can be said that overall, in economic terms, things are fine. Recent consumer-spending numbers suggest that as well. Retail sales in August were up 5% from a year ago, and total U.S. consumer spending this past quarter totaled $16.35 trillion — the highest level on record.

That doesn’t mean things are “fine” for everybody. Lower-income households are still contending with the elevated cost of living that five years of higher inflation has brought. It’s also important to keep in mind that the majority of spending is driven by more wealthy Americans. It’s likely lower-income households are leaning on ‘buy now pay later’ (BNPL) options when shopping online. In fact, Klarna, the biggest player in the BNPL arena, just became a publicly traded company this month. Making payments to purchase a car makes sense. Making payments to purchase dinner is scary. This does not bode well for the future.

Ultimately, while financial strain among lower-income households is troubling, it may not be the immediate risk to the U.S. economy. The top earners who drive the majority of consumption remain cushioned by wealth in stocks and real estate, and it would take a significant reversal in those markets to materially dent aggregate spending.

The most pressing hurdle facing the economy is still the uncertainty around tariffs. Will they ignite inflation or hurt corporate profits or slow the economy? Or be a total non-event?

What we do know is that tariffs are creating uncertainty today for businesses and consumers. For now, spending continues, and the economy keeps rolling. But the legality of whether a president can levy tariffs is headed to the Supreme Court, which means this story is far from over.

Next month, our Investment Commentary will be presented as a live webinar, airing on October 22nd at 1 PM CDT. You won’t want to miss it. Invitations will be sent out closer to the date.

This information is provided for general information purposes only and should not be construed as investment, tax, or legal advice. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable but is not guaranteed.