The headlines from the Iran conflict have started to fade. Stocks have recovered, and life feels like it has mostly returned to normal. But the war in Iran and the disruption in the Strait of Hormuz continue to leave energy markets unsettled. As we discussed in our March Investment Commentary and recent webinar, the Strait is a major global choke point for oil, natural gas, and other critical commodities. With shipping through the Strait effectively banned, the world continues to battle a massive energy supply shock.

That supply shock has raised the cost of energy. As a result, the inflation rate has accelerated to 3.8%, its highest level in three years

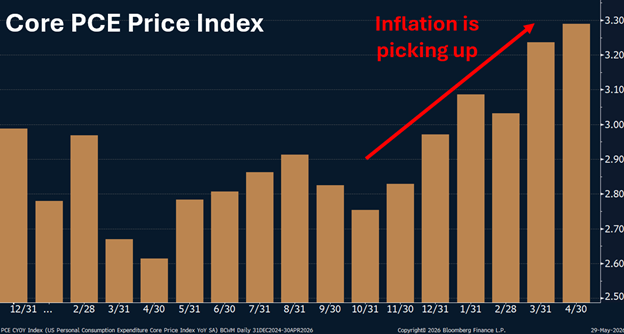

You may say, “Yeah, but strip out the rising energy prices, and it would look a lot better.” There’s a measure that does just that (strips out volatile energy and food prices from inflation). It’s called “core inflation.” And you can see the underlying pressures building in “core” prices (remember . . . oil touches everything). Core PCE, the inflation gauge most closely followed by the Federal Reserve, is starting to tell a story.

That is, inflation is picking up. And the unpopular task of raising short-term interest rates to curb inflation is on the table.

And who just showed up on the job? Kevin Warsh, President Trump’s newly installed Fed chairman.

For years, Trump has argued that the Fed should be lowering rates to support growth, and many Fed observers expected Warsh to be more sympathetic to that view. But Warsh now inherits a much harder problem: inflation is moving the wrong way, just as the White House wants more accommodating monetary policy.

Federal Reserve policy is supposed to be independent of White House influence, and Trump recently softened his tone in support of that independence. However, inflation pressures could persist and it would not be uncharacteristic for Trump to renew his demands for lower interest rates. That could leave Warsh stuck between a rock and a hard place . . . and create plenty of drama for CNBC headlines.

For now, most financial news is focused on whether the U.S. can reach a peace deal with Iran and reopen the Strait of Hormuz. But even if the Strait reopened today, the energy disruption would take time to unwind. Ship crews, insurers, and oil field workers all need confidence that the peace will hold. Oil production also cannot simply restart overnight, especially where infrastructure was destroyed by airstrikes and must be repaired or rebuilt.

We expect this bout of elevated inflation to be transitory but it will not be fixed overnight. Interest rates, and therefore bond prices, have reacted accordingly. Rates moved higher after the war broke out and we would not expect them to come back down to pre-war levels until there is meaningful progress toward a peace deal.

Ironically, stocks have largely looked past the energy-market disruption. Rising corporate profits and massive AI investment have helped push the S&P 500 Index to all-time highs. While we think the market is justified in looking through short-term inflation concerns, it may be leaning a little too hard into the AI trade, because right now the S&P 500 Index is “expensive” . . . especially relative to the interest rate you can earn on bonds.

One way to compare the attractiveness of stocks and bonds is to look at the profit companies generate relative to their stock prices (what we call the “earnings yield”). For example, a company earning $5 per share with a $100 stock price has an earnings yield of 5%. A higher earnings yield is more attractive because it means investors are getting more profit for the price they are paying.

If stocks are “earning” 5%, and bonds are paying you 4%, stocks may look more attractive. That 1% “spread” is positive. But when the earnings yield is 3.5% and bonds are paying you 4.5%, as they are today, the spread is negative, and bonds begin to look more attractive (see chart below).

For the last 20+ years, the spread has been positive (stocks typically yield more than bonds). Not so today.

The takeaway? This chart is screaming, “sell stocks and buy bonds.” That signal could turn out to be wrong, stocks could get even more expensive, but let the buyer beware.

Speaking of hot stocks, one of the world’s largest companies is making its shares available for purchase by public investors next month. SpaceX, the rocket company founded by Elon Musk in 2002, is expected to become the largest Initial Public Offering (IPO) in history, at a valuation approaching $2 trillion.

There is an initial registration form called an S-1 that companies must file with the Securities and Exchange Commission before going public. It provides potential investors with information on the company’s financials, business model, risks, etc. SpaceX’s S-1 reads like a science fiction movie.

Page seven of the document outlines the company’s mission, which is “to build the systems and technologies necessary to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars.”

It is hard not to admire the ambition. SpaceX is effectively telling investors they are trying to help humanity become an interplanetary civilization.

But as an investor, you want to know how the company is going to turn a profit today. And what the S-1 revealed is that the path to Mars currently runs through monthly internet subscriptions and infrastructure for Artificial Intelligence (AI).

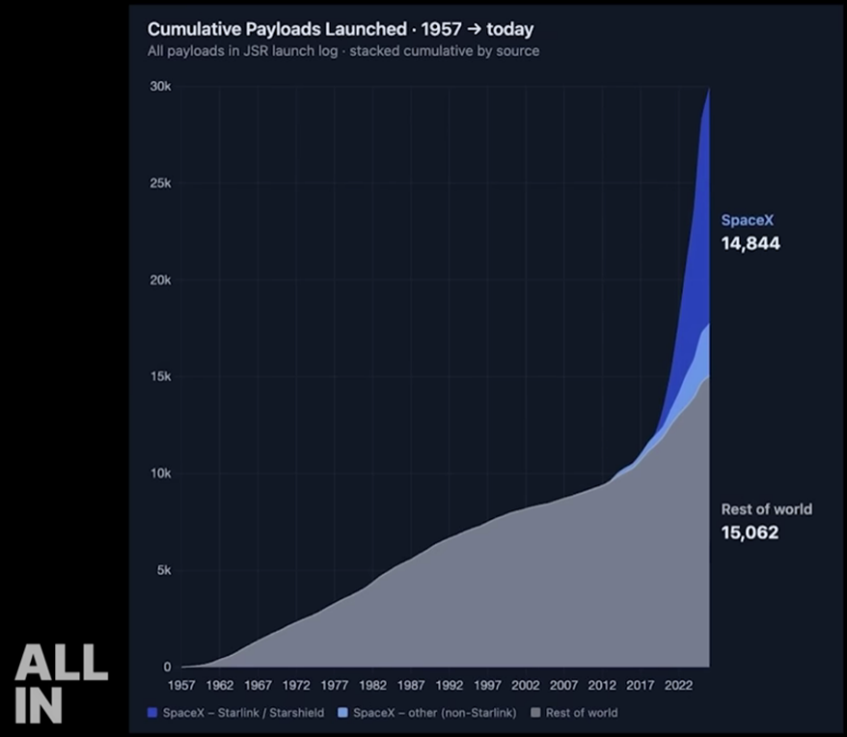

Since 2012, SpaceX has launched more than 14,800 payloads into space, nearly matching the number deployed by the rest of the world since the dawn of the space age.

These satellites enabled SpaceX to create the Starlink internet network, which, according to the S-1 filing, currently has over 10 million global subscribers and an annual revenue of $11 billion.

The cash flow from the internet business is now helping fund massive investments into data centers and AI infrastructure. Through its subsidiary SpaceXAI, SpaceX is currently selling computing power to Anthropic (a leading AI company and creator of Claude) to the tune of $1.25 billion per month.

So, the company used rockets to launch Starlink, it is using the revenues from Starlink to fund its AI investments, and it plans to parlay the AI revenue into a human presence beyond Earth. By the way, Elon’s pay package is contingent upon establishing “a permanent human colony on Mars with at least one million inhabitants.”

How exactly do you value a company like this?

Is SpaceX worth a premium because it owns the world’s most dominant satellite network? Because it may become one of the largest AI infrastructure providers? Or because investors are willing to pay for the possibility that the company eventually creates entirely new industries?

That uncertainty is part of what makes this IPO so compelling. But it is also what makes it risky.

Only about 5% of the company’s shares are being sold to the public. With such a limited supply of stock available, demand can push up the price so much that it quickly detaches from fundamentals, i.e., trades for a whole lot more than it’s worth. Millions of investors suddenly competing for a tiny slice of one of the world’s most fascinating companies can create the type of frenzy not seen since the Taylor Swift Eras Tour tickets went on sale.

If you want to purchase shares the day they go public, we would caution you to wait. Reuters recently analyzed the 50 largest IPOs of the past five years and found that, despite enormous hype, most companies ultimately underperformed the broader stock market over time. Investors would have generally done better simply buying the S&P 500.

It makes sense. By the time a company becomes “the most anticipated IPO in years,” expectations are often already exceeding perfection.

None of this means SpaceX will fail. The company is already changing the world. But history suggests that when investors fall in love with a story, they often end up paying a very high price for it.

At BCWM, we enjoy stories like this. And who knows, the IPO may turn out to be a great opportunity for investors. But our job is not to chase the most exciting story in the market. It is to weigh the opportunity and the risk. And in this case, the risk is hard to ignore.

This information is provided for general information purposes only and should not be construed as investment, tax, or legal advice. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable but is not guaranteed.