UPDATE: Immediately after we wrote this commentary, President Trump announced a five-day pause on strikes against Iran to allow for talks to end “hostilities.” Iranian officials denied any direct communication, but markets reacted anyway. Oil dropped from nearly $100 to $85 per barrel, stocks jumped roughly 2%, and interest rates moved noticeably lower.

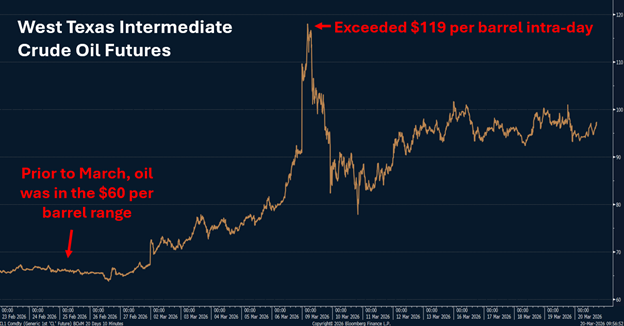

The biggest wild card resulting from any skirmish in the Middle East is OIL, OIL, OIL. Prior to March 1st, the price of a barrel of oil was in the mid $60s. On March 8th, it traded at almost double that . . . a move that typically takes years, not days.

For those living under a rock . . . on February 28th, President Trump ordered the U.S. military to attack Iran, escalating tensions in a region that has long served as the pressure valve for global energy markets.

The reason this war has so rapidly impacted markets has everything to do with the Strait of Hormuz, a tiny little opening in the Persian Gulf between the Arabian Peninsula and Iran through which roughly 20% of the world’s oil passes. Since the war broke out, the vast majority of oil tankers are not able to travel through this very dangerous choke point.

The result is a “supply shock.” There is significantly less oil making it to market, but the demand for that oil hasn’t changed. And when the demand for any product exceeds the supply, the price goes up. In this case, it goes up a lot.

This oil shock has implications far greater than what you pay at the pump. Oil is used in everything – pharmaceuticals, fertilizer for agriculture, synthetic clothing materials (athleisure, anyone?), manufacturing chemicals, and all things plastic, just to name a few. If it’s not made from oil, chances are it was transported by a truck, train, plane, or ship that uses fuel derived from oil.

The concern is that oil prices will stay too high for too long and the cost to produce everything else will rise, driving up inflation. This fear has pushed interest rates up and bond prices down. It has also increased the risk of a recession, which has driven stock prices down 5% in one month.

But while a 5% drop is noticeable, it’s helpful to zoom out and realize the S&P 500 index is still up 17% over the last 12 months, even after this shock to markets.

If you are fearful of a continued selloff resulting from the conflict with Iran, the good news is that recent history has shown these shocks tend to be temporary disruptions and not economy killers. The Gulf War of 1990, the Iraq War of 2003, the Arab Spring of 2011, and Russia’s invasion of Ukraine in 2022 all coincided with oil price shocks that proved sharp but short lived. This resilience reflects the greater flexibility of the modern global energy system compared to earlier eras.

While the price of a barrel of oil is about $95 (at the time of this writing), keep in mind that we’ve been here before. The average price of a barrel of oil from 2011 to 2014 was about $95 and our economy grew and stock prices went up.

The other good news is that Donald Trump pays attention to the stock market. And with midterms coming up, there is little appetite in Washington for $120 oil. President Trump has shown the ability to walk back threats quickly and dramatically. Emotional investors who jump out of the market after Trump headlines cause a selloff frequently miss out on subsequent large upswings. Markets don’t wait for everything to feel safe again. They start bouncing back the minute things stop getting worse. Not when the news is good . . . just when it’s less bad.

That being said, the oil shock does come at a precarious time for the U.S. economy. The job market has been stagnant for a year. Inflation may or may not be improving, depending on where you look. And economic growth is decelerating. Things aren’t bad, but they’re not great, either.

At BCWM, we ended last year with a little more cash than usual, and as opportunities have presented themselves, we’ve put that cash to work – buying stocks at lower prices and bonds at higher yields. We do not have a crystal ball that tells us when this war will end, but we’re confident our focus on portfolio risk will help us steer our clients through this current bout of volatility and beyond.

On that note, we’ll be hosting a live investment webinar at the end of April – keep an eye out for your invitation.

This information is provided for general information purposes only and should not be construed as investment, tax, or legal advice. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable but is not guaranteed.